Credit Karma

1.0

- Address: Credit Karma, LLC, P.O. Box 30963, Oakland, CA 94604

Unfortunately, MikeCredit does not currently work with this lender, but don't worry, click on the button to find the best deals and options available for you.

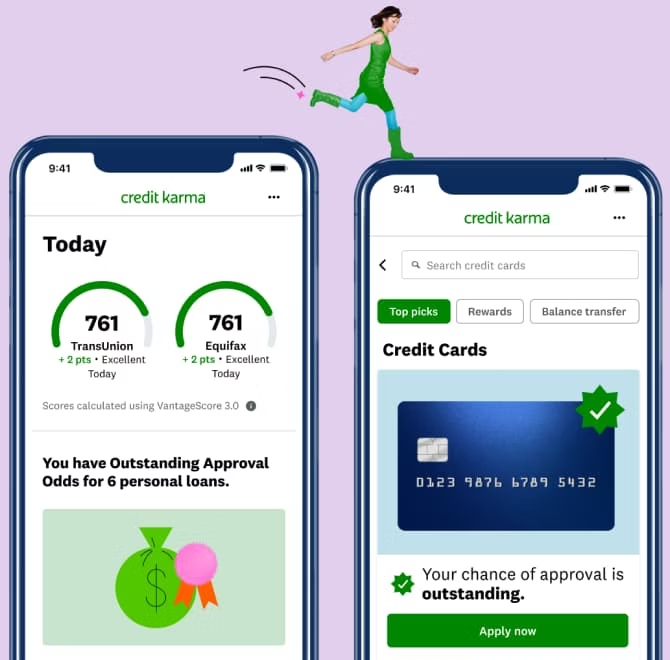

Credit Karma isn’t a traditional lender — it’s a free marketplace that connects you with different types of financial products: credit cards, bank accounts, savings, car loans… and personal loans.

Owned by Intuit, Credit Karma’s main business is helping you compare offers — they don’t lend money themselves.

They make money through partner commissions when a user signs a loan or credit product.

How to apply for a loan through Credit Karma

Here’s a simple step-by-step:

- Go to Credit Karma’s personal loans section — pick the “shop” tool.

- Enter some info — personal details like income, credit score, and how much you want to borrow.

- See your “Approval Odds” — Credit Karma shows a percentage that estimates how likely you are to be approved, based on its matching with other members.

- Compare real offers — you’ll get loan quotes from partner lenders: amount, APR, term, monthly payments.

- If you choose one, submit the full application — that typically triggers a hard credit pull, which can affect your credit score.

What types of loans you can find via Credit Karma

Credit Karma shows a variety of loan options, including:

- Short-term payday loans — for quick cash, but usually tiny amounts (often ≤ $500) and very short repayment windows.

- Payday alternative loans (PALs) — these come from credit unions, safer than payday loans: amounts from $200–$2,000, terms 1–12 months, APR capped around 28%.

- Unsecured personal installment loans — the more “normal” kind of personal loan, used for debt, emergencies, or larger expenses. According to Credit Karma’s offers, you can borrow up to $50,000.

Conditions: Amounts, Rates, Terms

Here’s what you’ll typically find on Credit Karma’s loan offers:

- Loan amount: Up to $50,000 on personal loans.

- APR (interest rate): From around 8.49% to 23.49% for some lenders (with AutoPay). Other lenders listed go up to ~35.99%, depending on credit.

- Term: Mostly 36 – 72 months (3–6 years) for installment loans.

- Fees: Credit Karma doesn’t charge you anything. But the lenders may charge origination fees or late fees.

pros and risks of Credit Karma loans

Advantages:

- Easy comparison — You can see many loan offers side-by-side.

- Soft credit check at first — so you can get pre-qualified options without hurting your score.

- No cost to use — Credit Karma doesn’t charge you anything for using their marketplace.

- Good for improving credit — If you also use their credit-score tools, you can track and learn how to make better decisions.

Risks / Things to watch out:

- Not a direct lender — Credit Karma only links to other lenders.

- Hard credit pull later — If you pick a loan and apply, the lender probably will do a hard check, which can lower your score.

- High APR for bad credit — Depending on your profile, you could be offered rates close to the top of the range (e.g., 30%+). Some users report very high APRs. > “I was offered a 23% interest rate … plus a new hard inquiry.”

- Data use / leads — Because Credit Karma makes money when you act on their offers, user data is passed to partner lenders. Some borrowers say they received spam or unwanted calls/emails.

- Pre-approval issues — Credit Karma has faced criticism (and a settlement with the FTC) for showing “pre-approval” suggestions that didn’t always guarantee approval.

Is Credit Karma a good option for you?

If you need fast money and don’t have many good credit options, Credit Karma can be a solid place to look. It’s especially useful for:

- Comparing personal loans quickly, so you don’t pick the first bad deal.

- Finding short-term borrowing options, if you’re okay with potentially very high APRs (but you should be cautious — payday loans can trap you).

- Checking your credit health, getting insights, and working on improving your score over time, so next time you borrow, you get better terms.

But — if you’re already very credit-impaired, or you don’t want to deal with very high interest, you might want to check credit unions or other more responsible lenders first.

Final verdict

Credit Karma’s loan marketplace is not a money-machine, it’s a tool. It doesn’t guarantee you’ll get a good rate, but it helps you shop safely, compare offers, and avoid predatory lenders more easily than going it alone.

For someone in a tight spot — living paycheck to paycheck, or with a poor credit history — Credit Karma is a decent first stop if you use it carefully. Always read the fine print, know how much you’ll repay, and make sure borrowing now won’t make your situation worse later.